63 US Banks on Brink! FDIC Blames Inflation, Not Bailouts

Free Market Fix Needed? Moral Hazard Created By FDIC Puts Banking at Risk.

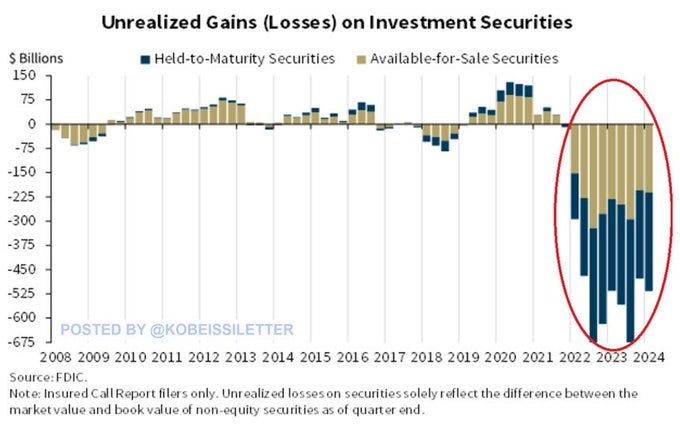

The FDIC has come out with its most recent report, stating that 63 U.S. banks are facing insolvency due to unrealized losses. In the report, the FDIC’s conclusion is, that “the banking industry still faces significant downside risks from the continued effects of inflation, volatility in market interest rates, and geopolitical uncertainty. These issues could cause credit quality, earnings, and liquidity challenges for the industry. In addition, deterioration in certain loan portfolios, particularly office properties and credit card loans, continues to warrant monitoring. These issues, together with funding and margin pressures, will remain matters of ongoing supervisory attention by the FDIC.”

The Federal Reserve and the FDIC's involvement in the banking system creates moral hazard and instability which is the complete opposite of their mandate. This situation highlights the need for a free market approach to banking and an end to consistently needing to bail out a banking system that clearly does not work for the long term. One thing the FDIC may do is simple window dressing, to instill confidence in depositors so they do not create a run on banks; however, that does not solve the fundamental issue of the U.S. banking business model.

FDIC deposit insurance encourages banks to take on riskier investments by reducing market discipline from large depositors and giving banks the impression that they are protected from the consequences of their actions via the government-backed FDIC. When depositors are protected, banks may have less incentive to monitor the performance of insured institutions. This can make funds available for weak institutions and high-risk ventures at a lower cost. FDIC research suggests that deposit insurance can lead to a decrease in market discipline from large depositors, which can increase risk-taking. Flat-rate deposit insurance can shelter banks from the true level of risk they are taking on, which can encourage poor decision-making.

What the government has done is create a “too big to fail” mentality, which distorts the market, allowing banks to believe that the government will always be there to have their back if all goes to hell. Instead of injections of taxpayer cash, what the banking needs is strong market discipline, so banks are more accountable to their depositors and depositors are more careful about where they deposit their funds.

We are reminded that before the FDIC there were wild swings in the banking industry with runs on the bank and many bank failures, yet the only difference today is that the taxpayers come to the rescue when the FDIC does not have the liquidity for large bailouts, so we print more money to shore up the banking industry as banks are continually in trouble.

If the FDIC were phased out, banks would be more cautious with their investments and would be more conservative with their business models. Instead of the distorted FDIC fees banks pay, banks would pay market rates for deposit insurance. Such a scenario would lead to an increase in competition and to more innovative and efficient banking solutions. It could also lead to expanded use of cryptocurrencies, such as Bitcoin, disrupting traditional banking.